Beyond the Budget: 5 Financial Blindspots That Are Costing You More Than You Think

1. The Hidden Architecture of Your Wallet

"Adulting" often feels like a series of high-stakes decisions made with insufficient information. Whether you are navigating the complexities of housing or trying to manage debt, the sheer volume of choices can be overwhelming. We are frequently told to "save more," but saving is only one pillar of financial health. Understanding the hidden mechanics of our financial system doesn't just save you money; it buys you peace of mind.

The true architecture of your wallet is built on underlying rules and regulations that govern how money moves. To help you navigate this system, this guide distills core principles from federal financial education standards into a "cheat sheet." Think of this as an insider’s look at the invisible forces that influence your credit, your housing, and your long-term stability.

2. Renting vs. Buying: The "1% to 4%" Maintenance Reality

Conventional wisdom often suggests that buying a home is the ultimate financial milestone. However, a sophisticated strategist looks past the pride of ownership to the reality of the balance sheet. While rent represents a "ceiling"—the maximum you will pay for shelter each month—a mortgage is merely the "floor."

According to federal housing guides, homeowners should budget between 1% and 4% of a house’s total value every single year just for maintenance and repairs. For a $250,000 home, this "hidden tax" of ownership amounts to 2,500–10,000 annually. Renters benefit from the transparency of a lease, whereas owners must maintain significant liquidity to handle the inevitable decay of physical property. Furthermore, there is a "time cost" that many busy professionals overlook.

Taking care of a home takes time. Generally speaking, the more house or yard you have, the more time it will take. While you may have some maintenance, decorating, or yard work opportunities in a rental, you will generally spend more time and money on these activities and items if you own your home.

Strategist’s Tip: If you lack the liquid savings to cover a 4% emergency repair, ownership may currently be a liability rather than an asset. Maintenance isn't an "if," it's a "when."

3. Your Credit Score is Actually a "Resume for Life"

Many believe credit scores only matter when borrowing money. In reality, your credit report functions as a "resume for life," and just like a professional CV, it can be "edited" through the dispute process if it contains inaccuracies.

Attempting a "cash-only" lifestyle (the "Yardley" scenario) can backfire. Without a credit history, you aren't seen as "frugal"; you are seen as an unknown risk. This often leads to higher security deposits for basic utilities and obstacles in daily life.

The following entities frequently check your credit resume:

Landlords: To set your security deposit amount.

Utility Companies: Electric, water, and gas providers.

Cell Phone Providers: To determine eligibility for service plans.

Insurance Companies: Depending on state law, this affects your premiums.

Employers: Crucially, federal law (Source 6) dictates that an employer cannot check your credit without your written consent.

Strategist’s Tip: Treat your credit report like a living document. Review it at least once every 12 months at annualcreditreport.com to ensure your "resume" is accurate and professional.

4. The 180-Day Grace Period: The Medical Debt Secret

A medical crisis is stressful enough without the fear of immediate credit destruction. Fortunately, medical debt behaves differently than a missed credit card payment. Nationwide credit reporting agencies generally will not report medical debt until it has been unpaid for at least 180 days.

This six-month buffer is vital for resolving insurance disputes and verifying charges. Perhaps the most empowering insight is this: unlike a standard late payment that lingers for seven years, medical debt that has been paid no longer appears on consumer credit reports. This unique "win" allows you to restore your credit health immediately once the bill is settled.

Key Takeaway: If you receive a medical bill, make sure it is valid. If you can’t afford to pay it, try to set up a payment plan.

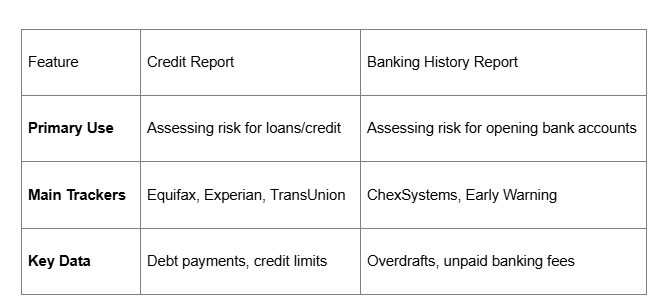

5. Banking "Background Checks": The ChexSystems Factor

While most people watch their credit reports, there is a silent background check happening every time you open a bank account. Companies like ChexSystems and Early Warning track your banking history, specifically looking for unpaid fees or overdrawn accounts.

If you are ever denied a bank account, you have a legal right to a free banking history report from the agency the bank used. For those with a spotted history, "Second Chance" checking accounts offer a path to rebuild your relationship with traditional banks.

Strategist’s Tip: You can proactively request your reports. Contact ChexSystems (800-428-9623 or chexsystems.com) or Early Warning (earlywarning.com) to see what banks see before you apply.

6. The Psychology of the Pay-Off: Snowball vs. High-Cost First

When tackling debt, you must choose between the mathematical winner and the behavioral winner.

High-Cost Debt First (The Mathematical Winner): You prioritize the debt with the highest interest rate. This is the most efficient way to save money on interest over the long term.

The Snowball Method (The Behavioral Winner): You pay off the smallest balance first. The "win" of closing an account quickly provides the psychological momentum needed to stay on track.

As a strategist, I recommend the Snowball method if you have struggled with consistency in the past. The dopamine hit of a zero balance is often more valuable than the interest saved if it keeps you from giving up.

Key Takeaway: Develop a plan to reduce your debt and get help if needed, such as from a trained credit counselor.

7. Conclusion: Your Financial Future is Not Your Past

The core philosophy of the FDIC’s financial standards is simple: Your credit history does not have to be your credit future. Whether you are correcting an error on a banking report or choosing a debt-reduction strategy that fits your personality, you have the power to reshape your trajectory.

Financial wellness isn't about perfection; it's about understanding the "invisible" rules and making them work in your favor.

Final Thought: If you could change just one "invisible" financial habit today—like checking your ChexSystems report or starting a 1% maintenance fund—which one would have the biggest impact on your 10-year goals?